National dwelling approvals continued to surprise – and for many, to delight – in December, with total approvals for 2020 lifting 5.5% to 183,769 dwellings. What will have pleased many in the building materials sector is the 15.1% rise in approval of free-standing houses, which lifted to 119,382 separate approvals. There is little doubt that low interest rates and the HomeBuilder program played a huge part in getting sales and approvals moving, but there are a couple of matters to watch over the remainder of 2021.

When the HomeBuilder program was introduced, the expectation was that it would provide sufficient fuel to drag underlying demand into the market. It would provide kick-along stimulus for a sector that was (around one year ago) expected to tank.

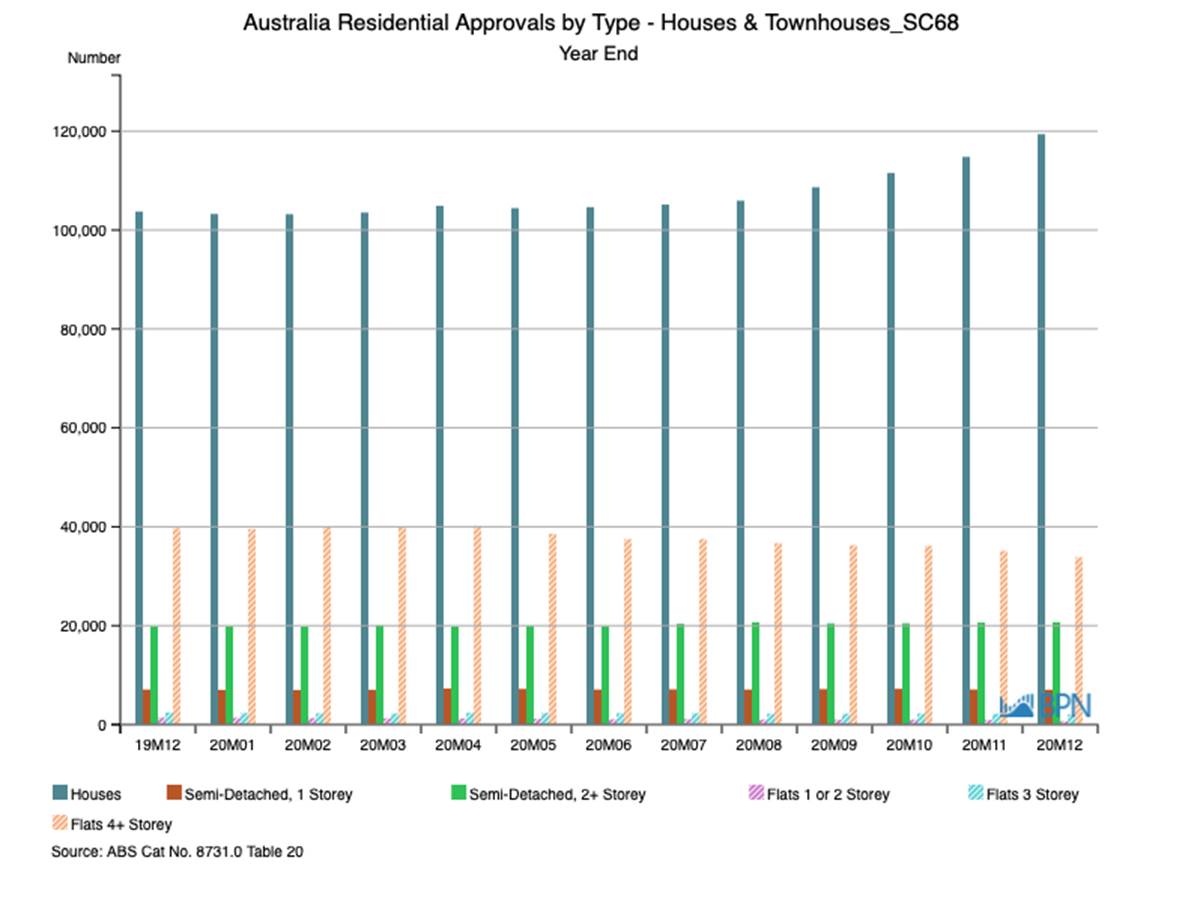

As we can see below, demand has not tanked, especially for free-standing dwellings. Month-on-month, annual approvals continue to grow, to the point where, by the end of 2020, they accounted for 65% of total dwelling approvals.

To go straight to the dashboard and take a closer look at the data, click here.

The table here sets out the good news for each of the last two years.

|

Format |

2019 |

2020 |

% Change |

|

Houses |

103,743 |

119,382 |

15.1 |

|

Semi-Detached, 1 Storey |

7,085 |

7,042 |

-0.6 |

|

Semi-Detached, 2 Storey |

19,834 |

20,706 |

4.4 |

|

Flats 1 or 2 Storey |

1,414 |

710 |

-49.8 |

|

Flats 3 Storey |

2,439 |

2,072 |

-15.0 |

|

Flats 4 Storey |

39,734 |

33,857 |

-14.8 |

|

Total Approvals |

174,249 |

183,769 |

5.5 |

The approvals data is very good news, but to some extent at least, it defies orthodoxy, if not logic itself. Why is this happening?

Doubtless, the stimulus measures are important in dragging demand forward, but how much of that demand is left, in an era when migration has ceased? There must be some upside effect from citizens returning home and needing housing, but it does not seem enough to provide for all the growth, especially with unemployment higher than pre-COVID levels.

Clearly, lower interest rates have been helpful. However, some caution is prudent. There is always a lag between approvals and construction starting and during which time some projects may not proceed. For instance, people who lose their jobs or do not have enough hours or money behind them are not being given houses, just Government stimulus to get them started.

So, that could flow through to the approvals that have already been booked. Some of them may not be built.

Still, there is a lot of demand coming to market and being approved, and there is little standing in its way right now.

If it is concerned about a ‘housing bubble’ – and given the steep rises in house prices over the last year, they well might be – the Reserve Bank of Australia (RBA) is not saying so at the moment. To paraphrase the ABC’s Ian Verender from a mid-February analysis, even if the housing economy is over-stimulated, the RBA is not going to act to rein it in.

When the stimulus comes off at the end of March, the housing economy could drop back down again. It probably will, and possibly should. But with interest rates at nowhere, the RBA cannot pull the interest rate lever and free up cash into the economy to stimulate growth. As we can recall from recent years – really since the GFC – whenever a Western economy did that, it did not work anyway.

The theory goes, according to Verender, that even though they were wealthier, those with lower interest rates did not go out and spend, because they did not feel wealthier.

This is the Wealth Effect. It works like any other irrational market sentiment: if house prices keep going up, or the stock market for that matter, then consumers and borrowers feel wealthier and keep spending, and making new housing commitments.

Now, because the sentiment is driving house prices up, it means those with existing assets are getting wealthier at the expense of those without housing assets. That sees two things happen. First homebuyers rush to get invested and are prepared to over-extend themselves. And on the other side of the ledger, those with assets become investors and jump into the borrowing queue to further expand their asset base.

Waiting for all this to happen is risky business of course. Where will it end?

Present demand at these levels is hard to explain given the decline in net migration, a traditional driver of household formation. In the absence of migration there is an actual limit to the amount of demand that exists in the economy.

While there is enough activity in the pipeline (refer earlier article) for new housing construction to remain strong during 2021 at some stage when demand begins to dry up, house price growth – and dwelling approvals will be slowed down. Probably that will not do much for those who are still without a place of their own at the end of this. For them, the dream will be further away, but that seems to be a problem for another day.

")

")

")