Inflation has been at the forefront of the economic narrative since interest rates started moving upwards in May 2022. At that time, inflation was running at 5.1% annualised, and peaked in December 2022 at 7.8%. In that context the 2023 September quarter rate of 5.4% continues the downward trend. However, to manage inflationary expectations, the RBA is forecasting inflation returning to its target band of 2-3% only by 2025.

As previously observed in Statistics Count, it is the pace at which inflation returns to the target range which is critical. In a recent speech, RBA Governor Michelle Bullock reinforced this point stating:

“Our focus remains on bringing inflation back to target within a reasonable timeframe while keeping employment growing. It is possible this can be done with the cash rate at the current level, but there are risks that could see inflation return to target more slowly than currently forecast. The board will not hesitate to raise the cash rate further if there is a material upward revision to the outlook for inflation.”

The concern in the September CPI data was the increase in the quarterly headline rate from 0.8% in the June quarter to 1.2% in September.

This potential change in trajectory and pace of movement toward the much-vaunted 2-3% inflation target was also evident in underlying inflation, where the quarterly trimmed mean increased from 1.0% in June, to 1.2% in September.

The main contributors to inflation in the quarter can be seen in the following graph which summarises the contributions by expenditure class on a weighted index points basis.

The big contributor is Automotive Fuel which the ABS advised was the largest quarterly rise in fuel prices since March 2022 and is mainly caused by higher global oil prices.

Significantly for the forestry and wood products industry, while prices for New Dwelling Purchases were the second largest contributor, they are now rising at a lower rate due to subdued demand for new dwellings and easing material costs.

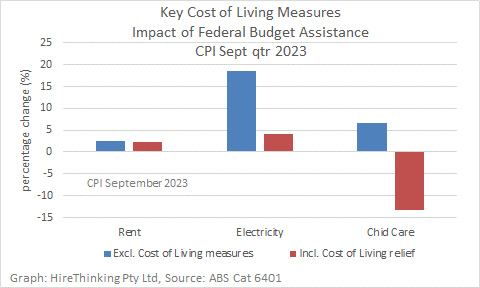

Interestingly, Rents and Electricity were the next largest contributors.

These have both been the subject of cost-of-living measures in the Federal Budget. The ABS commenting that from 20 September 2023, the maximum rate available for Commonwealth Rent Assistance (CRA) increased by 15 per cent in addition to the biannual CPI indexation that applies in March and September each year. Given the timing of these changes, the September quarter results show a partial impact of the CRA changes. On a straight percentage basis, rents rose 2.2 per cent in the September 2023 quarter with the increase moderated by changes to Commonwealth Rental Assistance. Excluding the changes to rent assistance, rents would have increased by 2.5 per cent.

Similarly, on a straight percentage basis, Electricity rose 4.2 per cent reflecting higher wholesale prices being passed on to customers from annual price reviews in July. However, electricity prices were partially offset by the Energy Bill Relief Fund rebates, which were introduced this quarter. The ABS observing that excluding the rebates, electricity prices would have increased 18.6 per cent in the September quarter.

The impact of Government cost-of-living measures was also evident with Child-care which fell 13.2 per cent, and was the largest contributing fall in September. The ABS observed that the changes to the Child-care subsidy raised the amount of subsidy received for over a million families and came into effect on 10 July 2023. Without the changes to the Subsidy, Child-care would have increased 6.7 per cent.

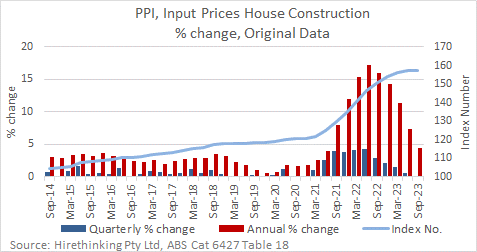

The Producer Price Index (PPI) provides more detail of the improving outlook for housing construction costs. Inputs to house construction were stable at 0.0% in the September quarter and well down on the peak in June 2022 when the QoQ% change was 4.34% and the YoY % change was 17.28%

It’s also noticeable that prices for Timber Building Materials are tracking about the same as other substitute products such as steel. In the September quarter Structural Timber declined -2.8% with Steel beams down -1.4% in the period.

A more detailed analysis of timber price movements is covered in the FWPA softwood weighted average price data series discussed elsewhere in this edition of Statistics Count.

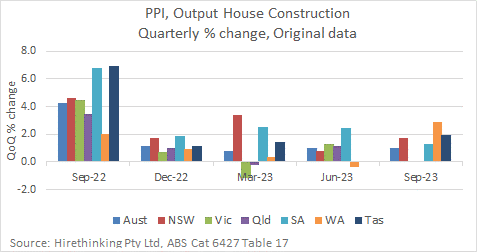

On a State by State basis, Victoria was well ahead of the pack, with the aggregate output price of house construction up only 0.06% in the September quarter, compared to growth in WA of 2.86% and NSW of 1.72%.

Just to hand the RBA has announced the 13th increase in interest rates in this tightening cycle to move the cash rate up a further 25 basis points to 4.35%. The markets were expecting this given the September CPI data discussed above suggests a “material impact” to the pace at which inflation returns to the target band expectations have increased.

In the statement accompanying the decision the RBA advised:

“CPI inflation is now expected to be around 3½ per cent by the end of 2024 and at the top of the target range of 2 to 3 per cent by the end of 2025. The Board judged an increase in interest rates was warranted today to be more assured that inflation would return to target in a reasonable timeframe”.

Tough news for mortgage holders and further indication of the fine line policy makers are juggling in achieving a soft landing for the economy.

")

")