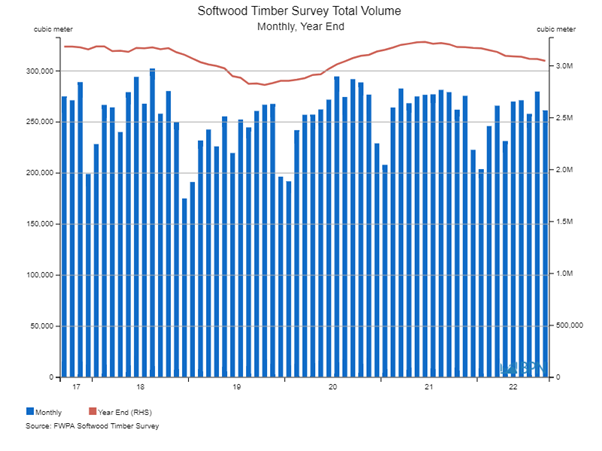

Sales of locally produced sawn softwood declined 5.0% year-ended September 2022, slipping to 3.048 million m3. The decline is almost 160,000 m3, with few grades in positive territory. The declines were led by the Export grade, which plunged 32.4% over the year. By contrast, Ungraded product lifted 6.0% over the same period.

As the first chart shows, local sales have been trending down for a little more than a year, but are shifting down very slowly and are well above the slump experienced in mid-2019. Market demand is not the primary challenge for local production. The fires of 2019-20 play a large role in the declining production, but so also do the supply chain and labour challenges that beset the entire economy.

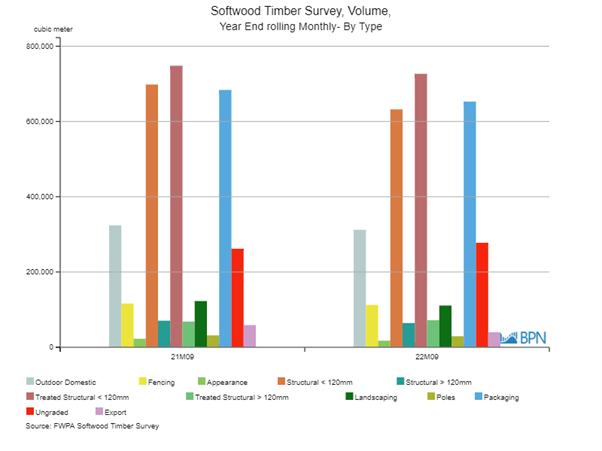

Sales of all product groups were lower over the period, except for the Ungraded volume and larger end Treated Structural >120 mm, which was up 5.2% over the year.

The chart below shows the comparative position for the last two years, but it is worth underscoring the result for the structural grades:

Grade YE Sep ’21 YE Sep ’22 % Change

Structural <120mm 698,282 632,257 -9.5%

Structural >120mm 70,591 64,432 -8.7%

Treated Structural <120mm 748,153 726,625 -2.9%

Treated Structural >120mm 68,285 71,859 +5.2%

The long migration to treated structural supply is continuing, with the differential now an aggregate of more than 100,000 m3 per annum.

")

")

")

")