All indications are the possible global recession is driving shipping costs lower as demand dries up. In a complex world where seemingly what can go wrong will conspire with whatever is already going wrong to create chaos, the rise of inflation around the world is dampening demand for goods and services across the world.

As the data below shows, shipping costs have plunged through 2022 and show little sign of stopping their free-fall. New contract rates are being negotiated at rates not seen since prior the pandemic.

Even the introduction of the mega alliances in container shipping has been unable to manage supply and demand to sustain prices. It is relevant however that the alliances appear to be regaining the market share they lost to smaller lines and ‘non-alliance’ carriers in the midst of the pandemic. Maritime Executive reports for example that after growing to around 40% of US West Coast traffic in 2021, by January 2023, that had fallen back to around 27% and looks destined to fall further.

This is important to comprehend because what the alliances offer is – in part – a stable and consistent pricing and scheduling structure. The non-alliance carriers offer service at a price.

As a consequence, falling demand feeds into churn of traffic back to the alliances and to lower average prices. This in turn reduces the cost of goods, which removes some of the inflationary pressures.

The point? Indications from the shipping sector are the upwards pricing pressures have dissipated at the beginning of the global supply chain, reducing the inflationary indicators for the forward market.

Writing in the Australian Financial Review, Emma Connors picked up this point saying that ‘tepid’ demand was ‘keeping a lid on the number of containers being shipped around the globe’. With about 80% of global trade in goods travelling by sea, all indications are that improvements are in the offing.

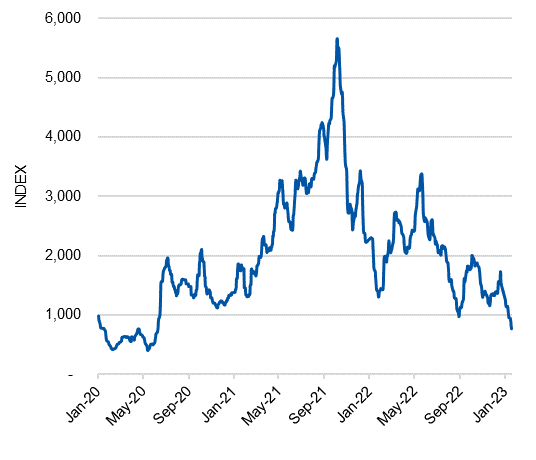

China Consolidated Freight Index (CCFI)

The China Consolidated Freight Index (CCFI) shows the cost of shipping finished goods from China around the world is now moderating.

Continuing the great freight roller-coaster, the average cost of containerized freight from China fell a huge 67.4% in 2022, having climbed almost as steeply in 2021. Remarkably, as the chart shows, by January 2023, containerised freight costs are largely back where they started two years earlier. A wild ride indeed!

From December to mid-January, the Australia/New Zealand route saw container freight costs decline a reported 10.4%. Welcome relief for those booking new slots right now.

China Containerised Freight Index: 3 Jan ’20 – 20 Jan ‘23

Similar to containerized freight, the main bulk shipping index – the Baltic Dry Index (BDI) – plunged 48.4% over 2022, measured in mid-January. It is now effectively at levels not seen since the start of the pandemic. Reports indicate the likely global recession is driving continued discounting by ship owners, which is likely to see the BDI fall lower in coming months.

Baltic Dry Index (Bulk Dry Shipping): 2 Jan ’20 – 20 Jan ‘23

Source: Bloomberg

")

")

")