It’s down, but how many more to come?

One could hear the collective sigh of relief across the country when the RBA announced on Tuesday, February 18th, to “…lower the cash rate target to 4.10.”

After 13 consecutive rate rises from 4 May 2022, when headline inflation was running at 6.1%, inflation came back to 2.4% in the December quarter.

Significantly, underlying inflation, as measured by the trimmed mean, was 3.2% annualised and 0.5% for the quarter. This was the lowest quarterly increase since June 2021.

Impact on Mortgage Holders – What the Rate Cut Means for Borrowers

Whilst it might not sound like much, the 0.25% reduction in interest rates will provide homeowners with a mortgage of $500,000 with a savings of around $81 per month. This should provide some relief in terms of interest payments to household disposable income. This appears to have peaked in the rate cycle at 7.76%, slightly lower than the 8.69% hit in June 2008 during the last rate cycle.

However, Reserve Bank Governor Michelle Bullock was quick to put the kybosh on further cuts, suggesting a wait-and-see approach. Concerns were flagged about the continued tightness of the labour market and uncertainty in global markets. The January unemployment rate was 4.1% seasonally adjusted, reflecting twenty-year lows.

The RBA forecasts are based on financial market interest rate predictions, with markets expecting four cuts over the next 12 months. On this basis, the February forecasts have been moved higher to 2.7% and above the November 24 forecast, which had the trimmed mean on track to hit the 2.5% mark.

Hence, Governor Bullock cautioned that “…if we cut too much too soon, then we might not get back to the middle of the inflation band.” So, at this stage, some easing is welcome, but overall, the Board is maintaining a “restrictive outlook.”

Nevertheless, this is good news for the housing sector, where historically, the level of interest rates has been a critical driver of housing affordability and, therefore, demand.

The pace of future cuts will be significant as Tarun Gupta, CEO, Stockland commenting in the Financial Review noted:

“We are anticipating a continued progression of more demand coming through but really need a number of cuts. If you look at past cycles, you know more substantial cuts in the 50-100 basis points range will then drive cyclically some very strong demand, because demand for housing is almost perfectly correlated with interest rates”.

Housing Sector Response – Assessing Market Trends and Affordability

It will take some time for the official housing data to reflect this reduction in interest rates. However, the available data indicates some strengthening of a weak base.

Building activity measures for the September quarter saw new house commencement of 28,043, up 5.2% on the previous quarter. Significantly, houses under construction were 87,672, down from a peak in March 2023 of 105,368. This was a decline of -0.7% in the previous quarter.

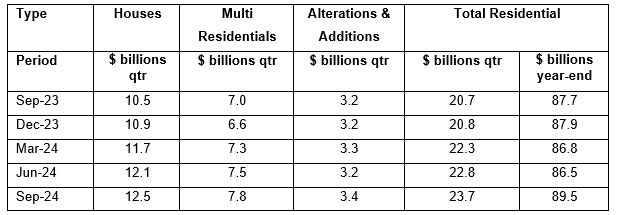

The value of building work commenced has stabilised and is trending upwards.

All sectors are up with houses each quarter for the past 4 quarters.

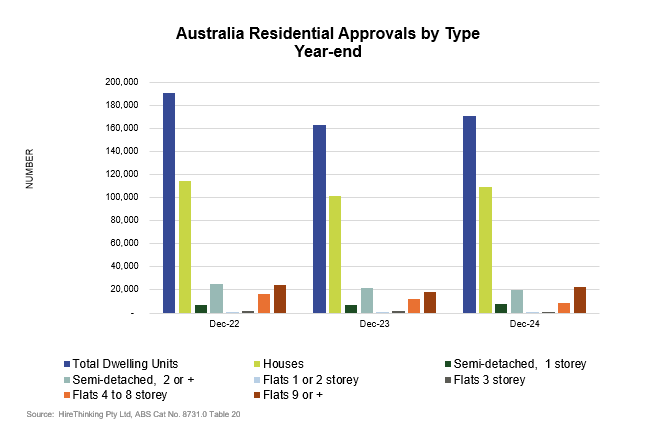

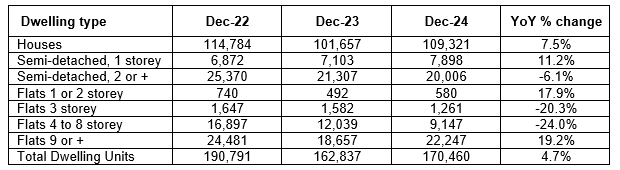

In terms of Housing Approvals on a year-end basis, we are starting to see some signs of life. Overall, total dwelling approvals in December were 170,460, up 4.7% from the previous period.

Housing has progressed and year-end December was 109,321 up 7.5% on the previous period.

However, the picture is not uniform across states. On a year-end basis there has been a big bounce back in WA where total dwelling approvals were 21,148 up an amazing 50.7%. Victoria, Queensland and South Australia also saw positive growth which NSW experienced a decline of -5.2%.

Future Outlook – Monitoring Economic Indicators and Potential Rate Movements

While this moves the market in the right direction from the decade-low level of approvals in 2023, it is still well below the level needed to reach the National Housing Accord target of 1.2 million dwellings over the next five years.

Subscribe to updates from FWPA’s Statistics and Economics Team:

To receive regular updates on data and analytics relevant to the forest and wood products industry, you can subscribe via this link.

")

")