Key points

• Total sawn softwood consumption edged up 0.3% year on year to just over 3.0 million m³, remaining broadly flat despite a strong lift in housing approvals.

• Domestic sawn softwood production (sales) rose marginally (+0.1%), while imports declined slightly ( 0.1%) to 618,317 m³.

• Dwelling approvals increased 9.0%, driven by multi unit construction, particularly apartments and townhouses.

• At a state level, the relationship between approvals and imports is uneven, highlighting timing lags, inventory draw downs and substitution between domestic and imported supply.

Housing market context

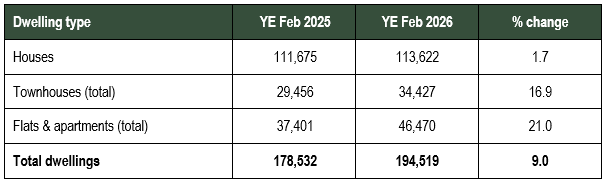

Total dwelling approvals reached 194,519 dwellings in the year ended February 2026, up 9.0% on the previous year. Growth was concentrated in medium and high density housing, with approvals for flats and apartments recording increases of between 46% and 111%, while approvals for detached houses increased only 1.7%.

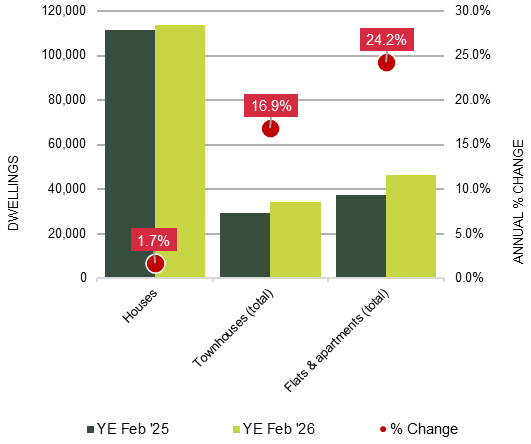

Australian Dwelling Approvals by Type: YE Feb 2025 v YE Feb 2026 (Number & %)

Source: ABS & IndustryEdge

This shift in dwelling mix has implications for timber demand, as multi unit projects typically use less untreated structural framing per dwelling than detached housing, but more packaging, treated and ancillary timber products.

Australian Dwelling Approvals by Type: YE Feb 2025 v YE Feb 2026 (Number & %)

Source: ABS & IndustryEdge

Sawn softwood consumption and production

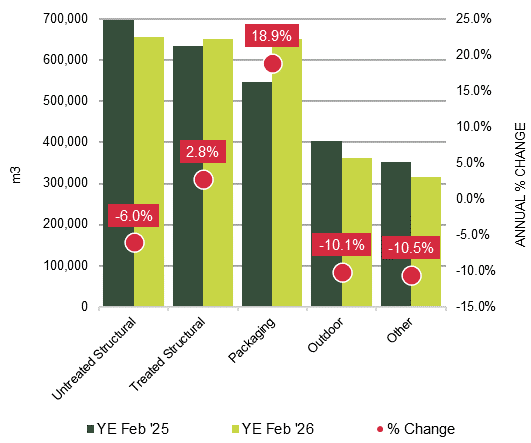

Total sawn softwood production (a proxy for domestic consumption) was 2.64 million m³ in YE Feb 2026, effectively unchanged from the previous year. However, there were significant changes within product categories.

Local Sawn Softwood Sales by Grade: YE Feb 2025 v YE Feb 2026 (m3 & %)

Source: FWPA & IndustryEdge

The decline in untreated structural timber, traditionally linked to detached housing, contrasts with strong growth in packaging, suggesting demand is being supported by non housing sectors and by higher density construction activity.

Local Sawn Softwood Sales by Grade: YE Feb 2025 v YE Feb 2026 (m3 & %)

Source: FWPA & IndustryEdge

Sawn softwood imports

Annual sawn softwood imports totalled 618,317 m³ year-ended February 2026, marginally lower than the previous year. Lower freight costs and softer prices supported imports, but volumes did not rise in line with housing approvals.

Imports by country

New Zealand increased its share of Australian imports to 28.6%, while imports from Germany and Estonia declined sharply.

Source: ABS & IndustryEdge

Imports by state

State‑level patterns show a mixed relationship between housing activity and import volumes. Queensland shows the clearest positive correlation between approvals and imports, while New South Wales and South Australia highlight substitution toward domestic supply, or potentially the use of existing inventories.

Importantly, however, there are limitations to the usefulness of these correlations because supply flows relatively freely across the nation – especially the eastern seaboard – regardless of the state in which imports are received.

Dwelling Approvals & Sawn Softwood Imports by State: YE Feb 2025 v YE Feb 2026 (%)

Source: ABS, FWPA & IndustryEdge

Note: NT and ACT excluded, due to receiving zero imports over the reference periods

Linking housing activity and sawnwood demand

Despite a clear recovery in housing approvals, sawn softwood consumption has remained flat. As has been widely discussed in the Australian industry, several factors may explain this divergence:

- Timing effects: approvals lead construction activity by several months.

- Dwelling typology mix changes: growth in flats and apartments reduces demand for structural timber on a per dwelling basis.

- Inventory management: builders, wholesalers and merchants may be drawing down existing supply chain stocks, rather than immediately increasing purchases.

- Supply substitution: alternative building systems, including steel, appear to have offset potential for growth in both local production and imports of sawn softwood.

Overall, the data suggest that while the housing market is strengthening, the transmission of that growing demand into sawnwood demand is proving to be slower and more complex than in previous housing cycles. Increased ‘noise’ created by multiple competitive circumstances detracts from the clarity that aids business and supply chain level decision making.

Pipeline shows worrying signs of a housing sector failing the nation

A successfully domestic housing sector meets national needs by linking demand with capacity, represented by dwellings being completed in a timely manner.

Prior to the pandemic, there was a reasonable expectation in Australia that from approval to completion, a free-standing house would be available to the purchaser in around 7.5 months. In 2024-25 the average was 11.5 months (ABS), while from commencement to completion, it was approximately 9 months.

The latter number is important because it emphasises that not all the constraints are driven by regulation and compliance. Equally relevant is that although Townhouses (14-15 months) and Apartments (33 months) take longer from approval to completion than houses, they are by their very nature delivered in multiples – sometimes in large numbers from a single construction activity.

In 2025, the number of Houses completed fell by 1.2% to 110,270, while the number of ‘Other’ dwellings (Townhouses, Flats and Apartments) completed fell by 4.8% to 61,840, compared to 2024. In 2025, total dwelling Commencements hit 195,300, up a solid 16.4% on 2024. However, total completions fell 2.5% to 172,110, meaning dwellings Under Construction lifted 11.3% to 235,885.

Demand for dwellings is clearly strong, but supply capacity continues to lag significantly, to the national detriment. This poor housing sector productivity is led by the traditional approaches to building. Many appear no longer to be fit for purpose. This factor also appears to be having a significant impact on demand for sawn softwood.

Disruption dominates near-term outlook

If elevated approval levels translate into higher commencements and completions through 2026, demand for structural sawnwood should be expected to lift gradually. However, the current mix of housing types and ongoing supply‑chain adjustments indicate any recovery in sawnwood consumption is likely to be incremental and patchy, rather than rapid and consistent.

")

")