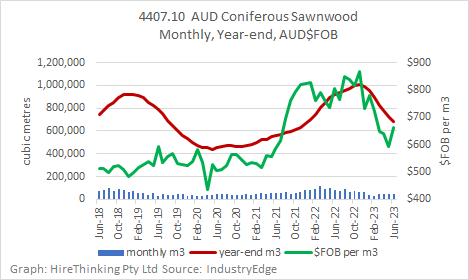

Overall softwood imports 4407.10 saw a continuation of the trend which commenced late 2022 of easing volumes. Volumes for the year-end June 2023 were 685,532m3 down -25.8% with a slight uptick in prices at $660.82 FOB per m3. This was a monthly rise of +11.5% but down from a peak in this cycle of $867.53 FOB per m3 which was in November 22.

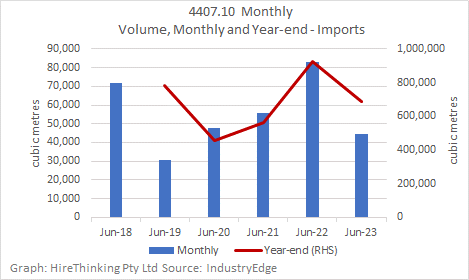

On a monthly basis, imports for June were 44,691m3 which was the lowest June monthly total since 2019 when imports were 30,412m³.

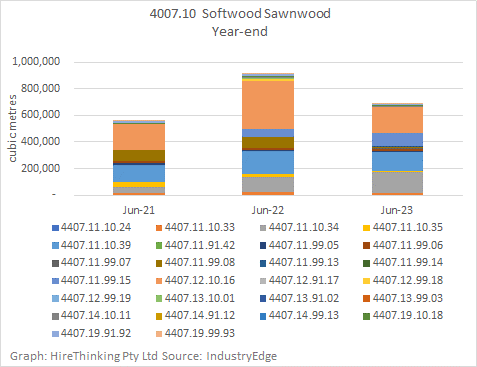

Of the 26 products covering softwood imports there were 4 products which represent most of the volume.

4407.11.10.34 (152,905m3 +40.8%) – Treated Other

4407.11.10.39 (141,572m3 -18.0%) – Other, Coniferous Untreated

4407.11.99.15 (98,333m3 +83.4%) – Other, not radiata pine, Roughsawn

4407.12.10.16 (195,256m3 -46.9%) – Coniferous wood of Fir or Spruce, Dressed

Although overall volume was down two of the main products increased during the period. It is also interesting to note three smaller products experienced significant increases in volume during the 12 month period (albeit of a low base). These were:

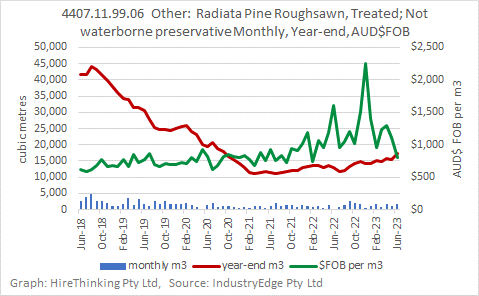

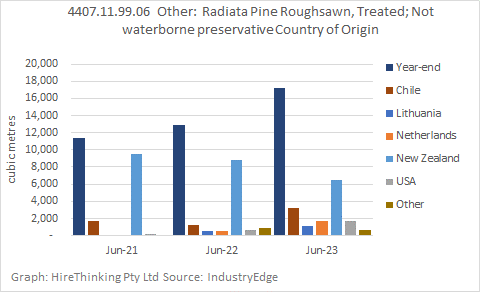

4407.11.99.06 (17,247m3 +34.0%) -Other: Radiata Pine Roughsawn, Treated

4407.11.99.07 (8,959m3 +138.4%) – Radiata Pine Roughsawn cross section <120cm2

4407.11.99.13 (4,895m3 +119.2%) – Radiata Pine Roughsawn cross section of 120cm2> or <450cm2

NZ is the main country of origin for all three products but as we can see with 4407.11.99.06 other countries have also contributed supply.

The increase through the past 12 months has seen supply from New Zealand complemented by increased supply from Chile (3,185m3 +152%), Lithuania (1,103m3 + 121%), Netherlands (1,693m3 +224%), USA (1,763m3 +159%).

It will be interesting to see in coming months whether imports of these products continue to grow and complement the “big 4”.

")

")

")

")