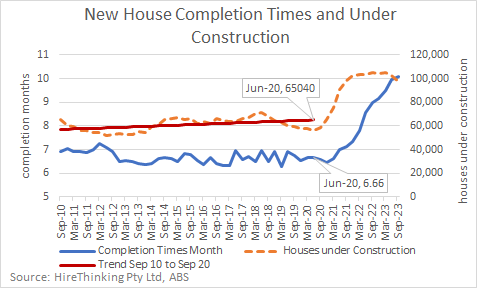

Reflecting more than a year of slowing approvals, latest data shows houses under construction (work in progress) contracted for the second successive quarter. However, analysis demonstrates that the expectation it is taking less time to build a house as a result is incorrect. In the September quarter, house completion times pushed out to 10.08 months!

The quarterly Building Activity data series from the ABS is the ‘gold standard’ on what is happening on building sites across Australia, and at a macro level, it is difficult to walk past.

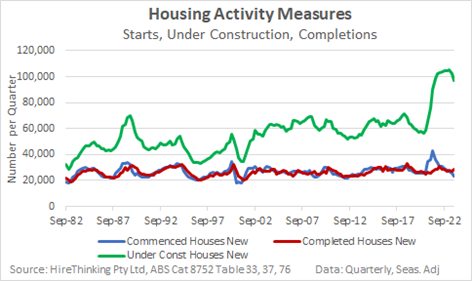

In that knowledge, we can assert with some certainty that analysis of this data shows there is generally a strong correlation between changes in houses under construction (green line) and changes in the time it takes to build a new house. Statistically if new home commencements (blue line) exceed completions (red line), then there is an increase in houses under construction (green line).

Similarly, if completions exceed commencements, then the number of houses under construction should decline.

This has been the case over the past two quarters, where the number of houses under construction has declined from a peak of 105,019 in March quarter 2023, to 93,120 in September quarter 2023.

Logically, if builders commence new house projects at a rate which accords with their capacity to build, then in general terms, commencements would match completions and houses under construction would remain relatively stable.

The explosion of houses under construction in the recent building cycle has been caused by the fact that completion rates have not increased to match commencements. If we look at the data pre-COVID and the incentive-fuelled boom during COVID, we can see demand overwhelming capacity.

Capacity – represented by completions – has barely moved over the better part of fifteen years, while commencements have lifted steeply, adding significantly to the average number of houses under construction.

| Av per quarter | Commencements | Completions | Houses under Const |

| Dec 2009-Dec 2019 | 27,223 | 27,028 | 61,141 |

| Mar 2020 – Sep 2023 | 30,476 | 27,519 | 88,358 |

The significant commercial impact of this imbalance between commencements and completions is that it takes longer to build the houses we do complete.

This has ramifications and reverberates throughout the supply chain, with builders being caught in what is often described as a ‘profitless’ boom. Some of this is reflected in timing, with fixed price contracts being outrun by availability, supply and cost of trades and other labour and of building materials. These time pressures have been exacerbated by the flow on effects of rescheduling, and in some cases costs of rework.

The overall causes are complex and many and are the subject of a new research project being undertaken by FWPA. The project to build ‘more houses sooner’ will look at industry supply chains, identify bottlenecks and model possible solutions.

As a result of the capacity constraints and the over-heating of demand relative to that capacity, completion rates in the current cycle increased to 10.08 months in the September quarter.

The statistical UFO identified here, is that historically, as the number of houses under construction eases, completion times start to decline. In this case, despite the past two quarters seeing houses under construction decline, this has not been associated with an expected decline in completion rates. This system feedback loop is delayed or disrupted, but, most worryingly, it may have shifted from one trend line to another, less desirable, trend, under which houses perpetually take longer to build.

There is the hope and for some, the expectation, that this is a timing issue and the disruption to the normal feedback loop will return over the course of 2024. That may well be the case because it would reflect the reality that many of the houses being completed were commenced a long, long time ago, in a galaxy far, far away, when fiscal stimulus to the housing sector waged war with the COVID invasion.

A return to the trend lines of the housing pipeline would be welcome right now. It’s a peace on which we could settle.

The trend line for industry capacity (reasonable balance between commencements and completions) suggests that 65,000 houses under construction with completion rates of 6.6 months being achieved is historically what industry can build. Assuming no other changes in capacity, it will be at that level that the contracts signed in the distant past will have washed through the system and a closer relationship between current demand and supply is experienced.

If that doesn’t prove to be the case, the identification of the statistical UFO will need to be met by assertive action to fix a system of work that will have proved itself broken and as Craig Francis wrote in Australian Property Investor, the outlook for the Federal Government’s five-year dwelling target will be bleak, if not entirely impossible to achieve.

")

")