Date: 31 July 2023

Locally produced sawn softwood sales declined 6.9% year-ended June, falling to 2.870 million m3. All products were down over the year, except the Export grade, which increased 47.6% over the full year.

As the chart shows, total sales continue to trend lower on an annualised basis, but the month-on-month sales declines are not as dramatic as over some earlier periods.

On a grade-by-grade basis, the data shows the pain has been almost universal, with a small (0.3%) rise in the Packaging grade and as foreshadowed, the large (47.6%) increase in the Export grade. While that sounds like the industry has rushed to the borders to find markets, the reality is that Export grade sales lifted from 39,202 m3 to 57,851 m3 year-ended June.

No sales are irrelevant but a lift of around 18,000 m3 over a year or an average 1,500 m3 per month is not especially significant.

The biggest declines have been recorded for Outdoor Domestic (-20.4%), the tiny volume of Appearance grade (-13.9%) and Treated Structural <120mm (-11.6%).

Against that backdrop, there may have been expectations of price shedding, but the latest data indicates the expectation has been misplaced.

Latest data shows prices for the main products remained relatively steady, down slightly for the quarter and down around 1.0% for the year.

The two large volume structural grades led the modest declines, as the charts shows.

Structural Untreated <120mm saw the Eastcoast weighted average down just 1.1% over the year-ended June, with the quarterly decline at 0.4%. Within that data, as the first chart shows, annual prices in Queensland are down 7.2%, but from a heady base. The other States appear more closely aligned.

The weighted average price for the June quarter was $746.85/m3.

The situation is similar for Structural Treated <120mm, where the weighted average price fell just 0.5% on an annualised basis for the Eastcoast, with the fall in the June quarter clocking in at 1.3%, underscoring – as can be observed below – that pricing has been solid for at least the last two years.

The weighted average price for the June quarter was $842.02/m3.

For each of the Structural Untreated and Structural Treated grades, the F4, F5 and F7 products recorded increased prices in the June quarter. Structural Untreated averaged quarterly price increases of 4.6%, feeding into total weighted average sales that saw prices increase 7.2%. The Structural Treated grade declined 2.2% for the quarter, exactly half of the annualised 4.4% decline.

There are few miracle products in the market right now, but there is doubtless some regard being shared for the strength of prices for sawn softwood packaging products.

Green Packaging prices were up 0.7% in the June quarter, feeding solidly into the annualised 1.9% average increase in prices. Although average prices were down 1.3% over the year-ended June in Victoria, they were, as the chart shows below, up 4.5% in NSW and 6.0% in Queensland over the same period.

The weighted average price for the June quarter was $374.09/m3.

The situation is only marginally different for Dry packaging, where weighted average prices were 1.4% lower for the June quarter and down 3.3% year-ended June. Annualised prices varied from a decline of 2.9% in Victoria to a sizeable 7.6% rise in Queensland, all of which was booked in the June quarter.

The weighted average price for the June quarter was $410.29/m3.

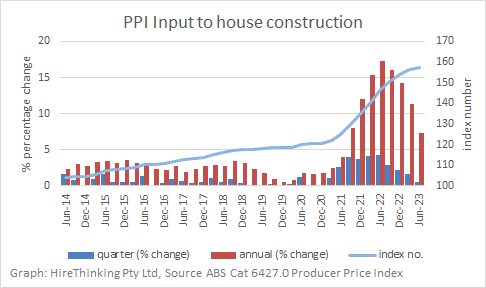

It is relevant to examine price changes for structural timber grades with the experience for major input prices to housing, here represented by the producer price index.

Input costs to housing lifted 0.6% in the June quarter and were up 7.4% for fiscal 2023, demonstrating that while costs were still increasing in 1H23, they were rapidly moderating.

The general PPI results for housing contrast with the declining prices being experienced for sawn timber.

Similar to the results recorded for sawn timber, the structural timber PPI was down 4.4% in on a year-on-year basis in June, contrasting with plywood and board (up 4.0%) and other metal products (up 6.8%).

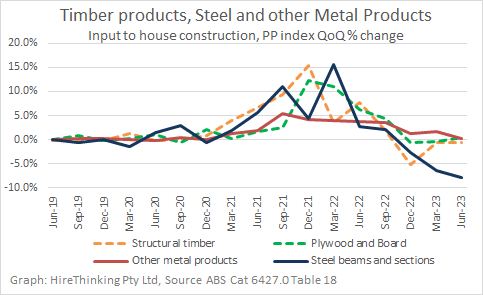

On a quarterly percentage change basis structural timber, plywood and board and other metal products remain relatively steady while steel beams and sections prices appear under greater pressure.

")

")